Decoding Batch Settlement Cycles in Acquiring Bank Systems and Their Effects on Financial Reporting Accuracy for Online Vendors

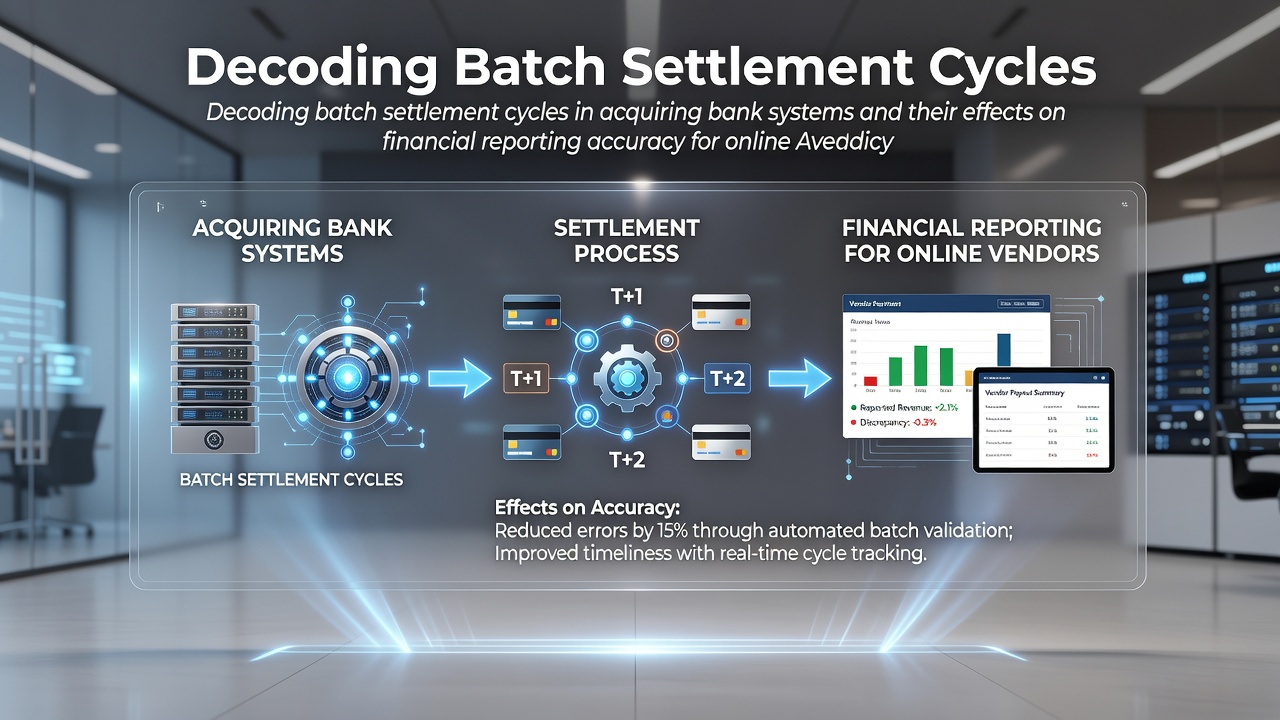

Batch settlement cycles operate as the backbone of transaction processing in acquiring bank systems where merchants submit groups of approved payments for final clearing and funding. These cycles typically follow daily cut-off schedules that determine when funds move from card networks through acquirers to vendor accounts and the timing creates measurable effects on how online vendors record revenue and reconcile accounts.

Mechanics of Batch Settlement in Acquiring Systems

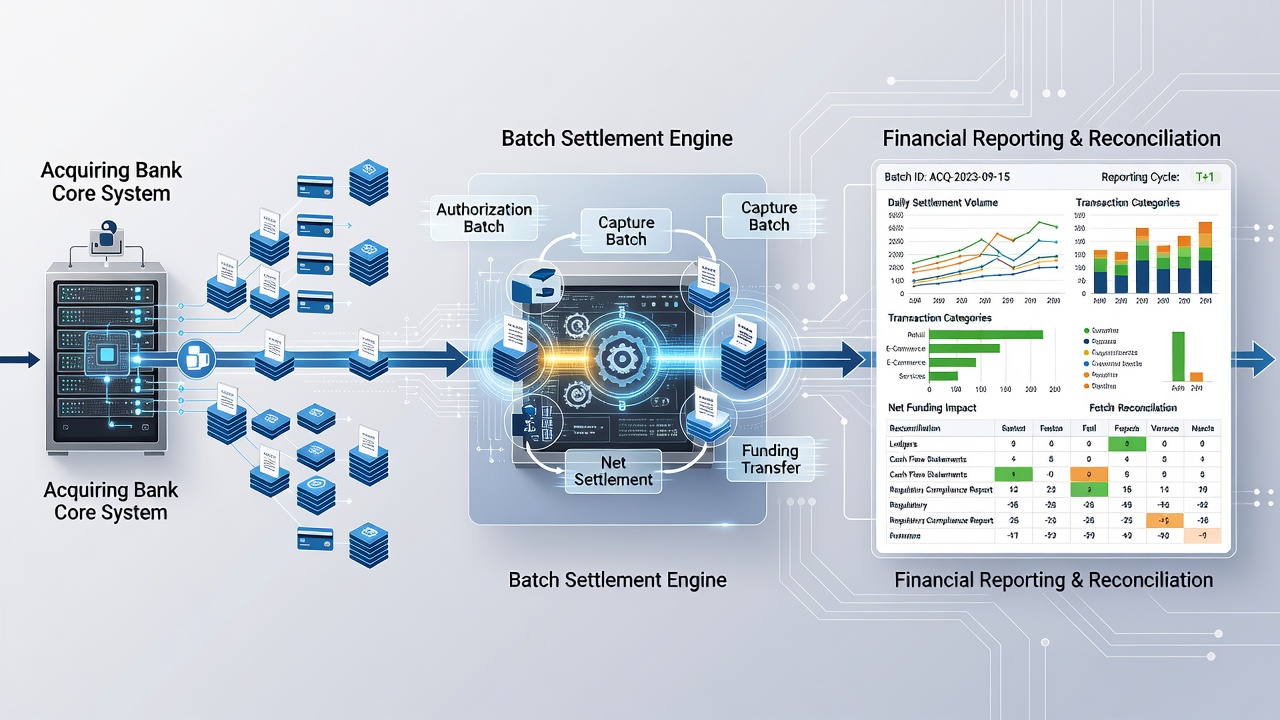

Acquiring banks collect transaction data from online vendors throughout each business day then bundle those records into batches for submission to card networks such as Visa and Mastercard. Network rules set specific processing windows and funds transfer occurs after authorization holds clear while interchange fees deduct automatically. Observers note that many acquirers run a primary batch close around midnight local time yet secondary cycles handle exceptions and international traffic on separate timetables.

Data from the Federal Reserve shows that electronic payment volumes reached record levels in recent years which places added pressure on settlement accuracy for vendors operating across multiple time zones. When batches miss a cycle due to technical delays or compliance reviews the funds remain in transit longer and vendors must adjust their internal ledgers accordingly.

Timing Effects on Financial Reporting Accuracy

Revenue recognition standards require online vendors to record sales when performance obligations complete yet settlement delays can separate the sale date from the cash receipt date by one or more business days. This separation forces finance teams to maintain detailed accrual entries that track pending settlements separately from cleared funds. Researchers at several institutions have documented cases where mismatched timestamps between gateway reports and bank statements led to temporary overstatements or understatements in monthly cash flow schedules.

Batch cut-off variations become especially visible during high-volume periods such as promotional events when transaction counts spike and exception queues lengthen. Those who've studied these patterns know that a single missed batch close can shift thousands of individual records into the next reporting period and require manual journal entries to restore alignment.

Reconciliation Challenges for Online Vendors

Online vendors rely on automated feeds from payment gateways to update accounting platforms yet acquiring bank settlement files often arrive in aggregated formats that omit granular per-transaction details. Finance staff must therefore cross-reference multiple data sources including authorization logs, batch summaries, and final funding advices to confirm that reported revenue matches actual inflows. Studies indicate that discrepancies frequently surface around month-end close when partial batches straddle reporting periods.

Payment processors sometimes apply rolling reserves or rolling holds that further complicate timing because those amounts settle on schedules independent of the main batch cycle. European Central Bank data on retail payment systems highlights how cross-border transactions experience additional settlement layers that extend the gap between authorization and funding by 24 to 72 hours in many instances. Vendors operating internationally therefore build buffer accounts in their general ledgers to absorb these timing differences without distorting periodic results.

Regulatory and Standards Context

Financial reporting frameworks such as IFRS 15 and ASC 606 emphasize control transfer over cash receipt yet settlement cycle documentation remains essential for audit trails. Regulators in multiple jurisdictions require acquirers to provide clear settlement reports that vendors can map to transaction dates and those reports became more standardized after updates rolled out in prior years. In June 2026 several networks plan to introduce enhanced batch identifier fields that should reduce mapping errors during reconciliation.

Industry reports from the Bank for International Settlements illustrate how improved data granularity in settlement files correlates with fewer restatements in vendor financial statements. Vendors that integrate settlement APIs directly into their enterprise resource planning systems report lower rates of manual adjustments compared with those relying on file uploads alone.

Practical Adjustments in Vendor Operations

Many online vendors implement automated reconciliation rules that flag transactions whose settlement dates fall outside expected windows and route those items for review. This approach reduces the volume of period-end corrections while preserving audit-ready documentation. Data indicates that firms adopting such controls experience measurable improvements in the accuracy of quarterly cash position forecasts.

Acquirers also publish cycle calendars that list daily cut-off times and holiday adjustments so vendors can anticipate delays and adjust posting schedules in advance. Those calendars prove particularly useful for subscription-based models where recurring charges must align with renewal periods without creating artificial spikes in reported receivables.

Conclusion

Batch settlement cycles in acquiring bank systems establish fixed timing parameters that directly influence the precision of financial reports prepared by online vendors. Clear mapping between transaction authorization dates, batch close times, and final funding dates allows finance teams to maintain consistent revenue recognition and accurate cash flow tracking. Continued standardization of settlement data fields along with direct API integrations supports ongoing improvements in reconciliation efficiency across the sector.