How Fraud Screening Outputs Shape Terminal Configurations Across Retail Networks

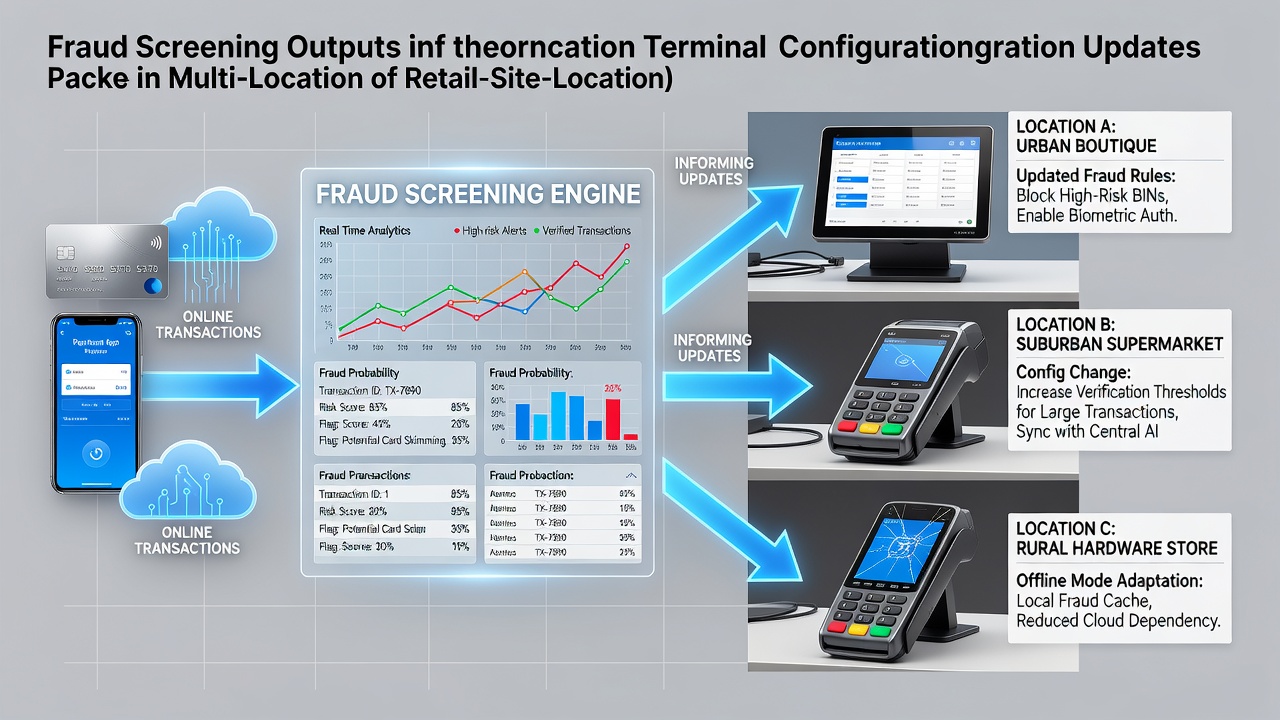

Retail chains operating both online storefronts and physical locations rely on integrated data pathways that connect digital transaction monitoring with in-store hardware settings, and these connections have grown more pronounced as payment volumes increased through mid-2026. Fraud screening systems examine online purchases for indicators such as mismatched billing details, unusual purchase velocities, and device fingerprint anomalies, then generate structured outputs that feed directly into configuration management platforms used by multi-location operators. Those outputs typically include risk scores, flagged attribute lists, and recommended rule adjustments that central teams translate into terminal parameters like authorization thresholds, address verification requirements, and transaction velocity limits. In July 2026 several large North American retailers completed phased rollouts of automated mapping tools that pulled live screening results into their point-of-sale firmware update queues, reducing manual intervention at individual store sites.

Retail chains operating both online storefronts and physical locations rely on integrated data pathways that connect digital transaction monitoring with in-store hardware settings, and these connections have grown more pronounced as payment volumes increased through mid-2026. Fraud screening systems examine online purchases for indicators such as mismatched billing details, unusual purchase velocities, and device fingerprint anomalies, then generate structured outputs that feed directly into configuration management platforms used by multi-location operators. Those outputs typically include risk scores, flagged attribute lists, and recommended rule adjustments that central teams translate into terminal parameters like authorization thresholds, address verification requirements, and transaction velocity limits. In July 2026 several large North American retailers completed phased rollouts of automated mapping tools that pulled live screening results into their point-of-sale firmware update queues, reducing manual intervention at individual store sites.Data Pathways Between Online Screening and Physical Terminals

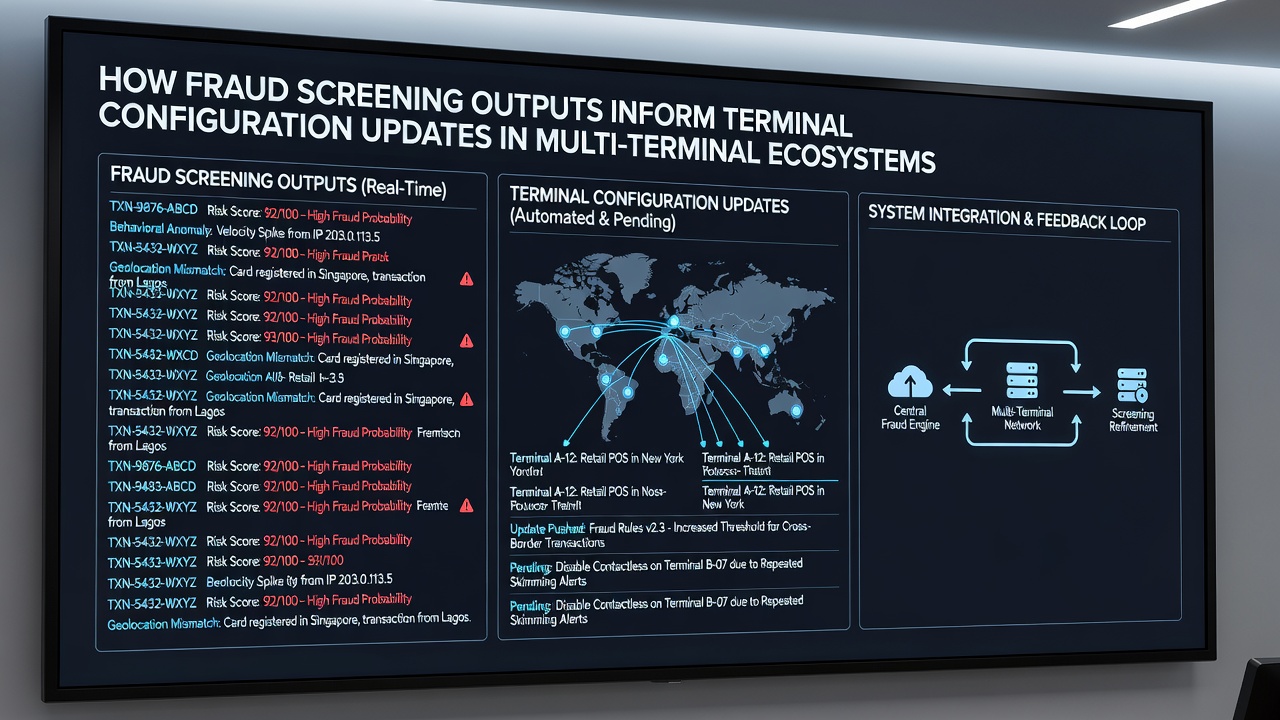

Transaction monitoring platforms capture screening decisions in real time, packaging them as structured messages that travel through secure APIs to enterprise configuration servers. Each message carries metadata about the flagged element, whether it was a high-risk IP address or a sudden spike in card-not-present attempts, allowing operations teams to correlate those signals with terminal behavior across regions. Middleware layers then convert the screened attributes into device-specific commands that adjust settings such as floor limits or mandatory PIN prompts without requiring on-site visits.

Multi-location operators maintain centralized rule repositories that receive nightly or hourly batches from the online screening engines, and those repositories push incremental updates to terminals during off-peak windows. The process maintains consistency because each location references the same policy baseline while still accommodating local regulatory variations, such as differing requirements for signature capture in certain Canadian provinces compared with U.S. states.

Configuration Updates Triggered by Screening Signals

When screening engines detect elevated fraud rates tied to specific card-present use cases, the resulting outputs prompt immediate changes to terminal profiles. For example, an increase in counterfeit card detections at self-checkout lanes can lead to lowered contactless transaction ceilings or the activation of additional cryptographic checks on the device firmware. Retail systems log each adjustment with timestamps and version numbers so that auditors can trace the origin of any given setting back to a particular screening event.

European retailers have adopted similar workflows following guidance issued by the European Payments Council, which outlined best practices for synchronizing risk signals across channels. One documented implementation involved routing screening outputs through an orchestration layer that validated each proposed terminal change against PCI DSS requirements before deployment, ensuring that security updates did not inadvertently conflict with existing compliance controls.

Operational Coordination Across Distributed Sites

Regional managers receive automated notifications when configuration changes are queued, and they can review impact summaries that list affected terminals by store identifier and current firmware version. The summaries also indicate whether the update originated from online screening patterns or from card-network mandates, helping teams distinguish between proactive fraud responses and mandatory compliance adjustments. In practice this distinction matters because screening-driven changes often carry expiration dates tied to the duration of observed threat patterns.

Inventory and loss-prevention teams monitor post-update metrics to confirm that the new settings produce the intended reduction in chargebacks. Data aggregated across hundreds of locations shows measurable drops in disputed transactions within 48 hours of synchronized terminal updates, according to internal reporting shared with the Federal Reserve Bank of Richmond payment research group. Those metrics feed back into the screening models, closing the loop between online detection and physical device behavior.

Technical Considerations for July 2026 Deployments

System integrators working with multi-location chains in 2026 emphasized the need for robust rollback mechanisms that could revert terminal configurations within minutes if downstream processing delays appeared. The same orchestration platforms that push updates also maintain versioned snapshots, allowing rapid restoration when a screening output contained an error or when a regional regulation changed unexpectedly. Testing environments replicate production terminal fleets so that proposed rule changes can be validated against sample transaction streams before live deployment.

Network latency between central configuration servers and remote sites remains a key variable, particularly for chains with locations in rural areas where connectivity fluctuates. Scheduled updates therefore incorporate staggered delivery windows that prioritize high-volume stores during the first wave and lower-volume sites in subsequent batches, minimizing the window during which any single location operates under outdated parameters.

Conclusion

The linkage between online fraud screening outputs and terminal configuration updates has become a standard operational component for multi-location retailers, supported by documented data flows, middleware translation layers, and compliance checkpoints that keep physical devices aligned with evolving digital risk signals. As screening engines continue to refine their detection capabilities and configuration platforms gain additional automation features, the synchronization process is expected to grow more granular while remaining traceable through audit logs maintained across distributed retail networks.