Retailers Discover Unexpected Benefits When Linking Payment Gateways to Fraud Detection in Recurring Transactions

Retailers have started connecting their payment gateways directly to advanced fraud detection tools, and this linkage has produced results that extend well beyond basic transaction security for recurring billing setups, while experts observe patterns emerging across subscription-based services and membership models. Data from multiple payment processors shows that these integrated systems catch suspicious activity in real time, yet they also deliver operational insights that help businesses refine their recurring revenue streams without adding layers of manual review.

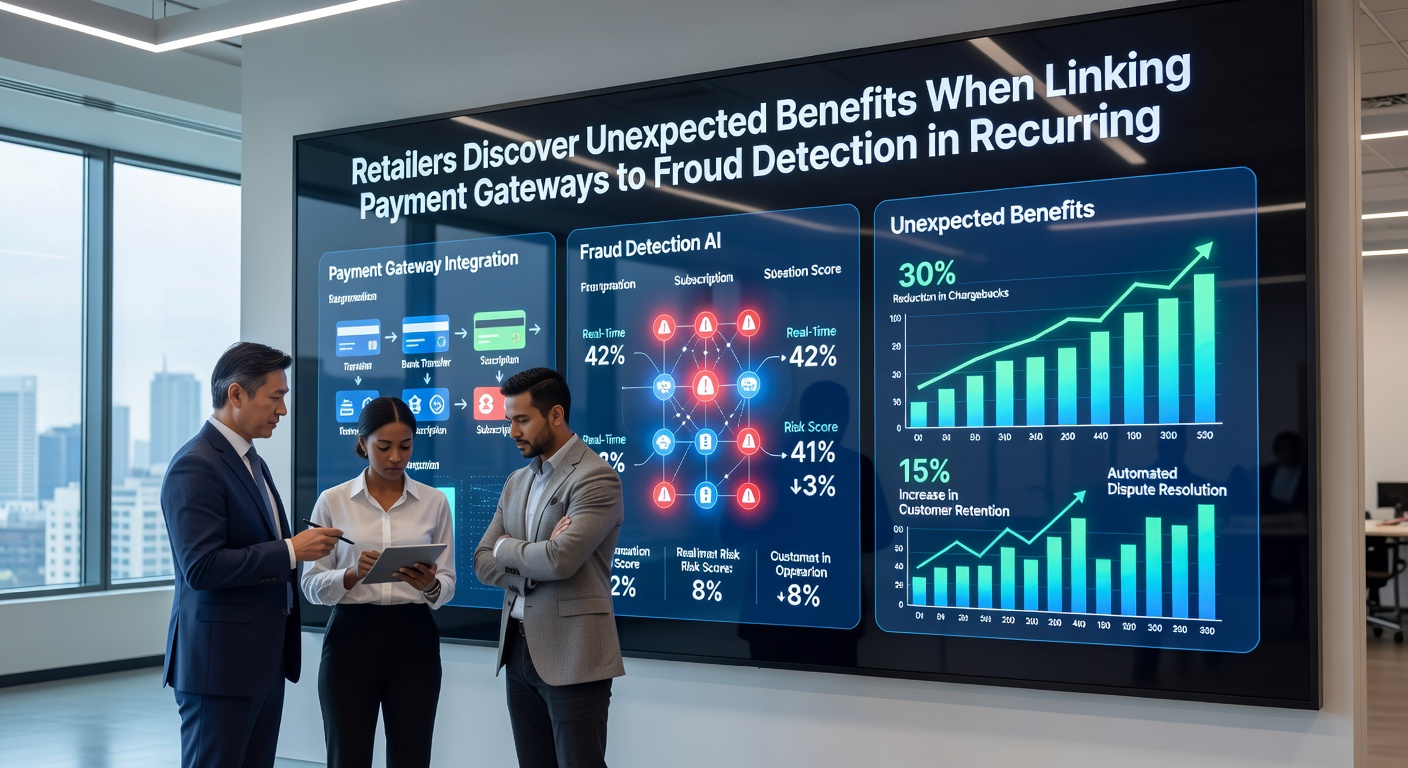

Mechanics Behind the Gateway and Detection Connection

Payment gateways serve as the bridge between customer accounts and merchant systems, processing everything from monthly subscriptions to automated renewals, and when fraud detection layers attach to these gateways they analyze patterns such as unusual IP shifts, device inconsistencies, and velocity checks across multiple billing cycles. Observers note that this setup allows algorithms to flag anomalies before they trigger chargebacks, while the connection simultaneously logs data points that reveal customer behavior trends over extended periods. Retail chains handling high volumes of recurring payments have reported smoother reconciliation processes because flagged transactions route automatically to verification queues rather than disrupting the entire batch.

Unexpected Operational Gains from Integrated Systems

Beyond reduced fraud losses, retailers have uncovered efficiencies in areas like inventory forecasting and customer segmentation, since the fraud detection modules generate detailed reports on transaction timing and geographic distribution that feed directly into business intelligence platforms. One study revealed that companies using linked systems experienced faster settlement times on legitimate recurring charges because fewer false positives interrupted the approval flow, and this streamlining freed up staff to focus on service improvements instead of dispute resolution. What's interesting is how the same data streams support compliance reporting, giving merchants clearer audit trails that align with evolving regulatory expectations in regions across North America and Europe.

Turns out the integration also supports predictive modeling for churn rates, as patterns in declined recurring transactions often signal upcoming cancellations long before customers reach out, allowing proactive outreach campaigns that retain revenue without increasing marketing spend. Retailers who adopted these connections in early 2025 noted that the combined gateway and detection environment cut processing costs by consolidating vendor relationships, since one platform handled both authorization and risk scoring rather than requiring separate services.

Data Trends and Industry Examples Through Mid-2026

Figures from the European Banking Authority indicate rising adoption of linked fraud tools among subscription merchants, with metrics showing a measurable drop in unauthorized recurring charges across EU markets during the first quarter of 2026. In May 2026 industry analysts released updated benchmarks highlighting how North American retailers achieved similar gains, particularly in sectors like software-as-a-service and utility billing where recurring volumes dominate daily operations. Researchers discovered that these systems also improve cross-border transaction handling by applying consistent risk rules regardless of currency or location, which reduces the complexity that once plagued international subscription models.

Take one mid-sized electronics retailer that integrated its gateway with real-time detection software and subsequently observed better alignment between payment success rates and customer loyalty program participation, since secure recurring billing encouraged longer subscription commitments. Observers note that the data collected through these platforms often reveals seasonal variations in fraud attempts, giving merchants advance notice to adjust verification thresholds during peak periods like holiday renewals.

Broader Impacts on Retail Strategy and Compliance

Linking these technologies has prompted retailers to rethink how they structure recurring offers, incorporating dynamic pricing adjustments based on risk profiles generated during the authorization process, and this approach maintains revenue stability while addressing potential vulnerabilities. Those who've studied payment networks know that the combined systems create richer datasets than either component alone, supporting everything from targeted retention offers to refined fraud rule tuning that adapts to emerging threat vectors. The reality is that regulatory bodies in Canada and Australia have begun referencing similar integrations in guidance documents, encouraging merchants to adopt unified platforms that satisfy both security and reporting requirements in one workflow.

Conclusion

Retailers continue to explore the full range of advantages that arise when payment gateways connect seamlessly with fraud detection capabilities tailored to recurring transactions, and ongoing developments suggest these linkages will influence future platform designs across the payments landscape. Evidence suggests sustained interest in these integrations as businesses seek to balance security demands with operational agility in an environment where subscription models keep expanding.